The Rivian Stock Surge: An Analysis of the Rally and Its Sustainability

Beneath the Surface of Rivian's Good Quarter

The market saw Rivian’s stock jump—up over 7%, to be more exact, 7.78% at one point—and reacted to a series of seemingly positive data points. Third-quarter revenue surged 78% year-over-year to $1.56 billion. The company posted its first-ever consolidated gross profit ($24 million). And the board locked in CEO RJ Scaringe with an ambitious new 10-year compensation plan. On paper, it looks like a clean bill of health for an EV company navigating a brutal market.

But these figures, while factually correct, are not the real story. They are lagging indicators, echoes of past decisions and temporary market conditions. Focusing on them is like judging the integrity of a skyscraper by admiring the lobby's marble floors. The real test of the structure is happening far above, where the steel is being bolted into place against the wind. For Rivian, that test is the R2 platform, and my analysis suggests that everything else is just noise. The market is cheering for a battle that’s already been won, while the war for survival has yet to begin.

Deconstructing the Profitability Mirage

Let’s dissect that gross profit. A positive gross margin is a critical milestone for any manufacturing company, signaling a move from selling every unit at a loss to potentially achieving scale. But the source of that profit is what matters. The company attributes it to its software and services business, which is a convenient and tech-friendly narrative. This segment, however, is a composite of two very different things: routine vehicle service work and a joint venture with Volkswagen.

The question is, how much of that $24 million profit was a repeatable, scalable metric, and how much was a one-time milestone payment from VW? The filings lack the granularity to make a definitive call, but this is the part of the report that I find genuinely puzzling. If the profit is primarily from the VW deal, it's less an indicator of operational efficiency and more a reflection of a successful capital partnership. It's good news, but it's financial engineering, not a fundamental shift in the cost of building and selling trucks.

Then there are the vehicle deliveries: 13,201 in the quarter. A strong number, but one the company itself admits is a "high-water mark" for the year, juiced by the expiration of government incentives. This isn't organic demand stabilization; it's a pull-forward effect. It’s an outlier, not a new trend line. Treating it as a sign of sustained momentum is a fundamental misreading of the data. The operational picture is improving, yes, but the foundation isn't nearly as solid as a single quarter's headline numbers suggest.

The Only Variable That Matters

Strip away the quarterly earnings beats and the incentive-driven delivery bumps, and the Rivian thesis boils down to a single, high-stakes variable: the successful launch and mass-market adoption of the R2 platform, slated for 2026. The company is essentially a rocket on the launchpad. The Q3 results are the final systems checks—all lights are green, the weather is clear, and the comms are good. But the rocket hasn't actually fired its engines yet.

With $7 billion in cash and short-term investments, Rivian has the fuel to get through the launch sequence. But the automotive sector is littered with the wreckage of companies that had enough cash to start the journey but not enough to finish it. The competition is no longer a nascent Tesla; it's every legacy automaker on the planet, all of whom are now pouring billions into their own EV platforms. Rivian had a head start, but the pack is catching up.

This context makes the board's new compensation package for RJ Scaringe look less like a reward and more like a high-stakes contract to see this one specific mission through. Tying his pay to audacious stock price targets and profitability goals is a powerful focusing mechanism. But is it a signal of the board's unshakeable confidence, or is it a form of golden handcuffs designed to keep the company's visionary founder lashed to the mast as it sails into the storm? What happens if the R2 launch is delayed or, worse, if it lands in the market with a thud? The plan aligns incentives perfectly for success, but it doesn't de-risk the venture itself.

The Data Is A Distraction

Ultimately, the market's positive reaction to Rivian's recent performance is a classic case of focusing on the wrong timeline. Analysts and algorithms are rewarding the company for tidying up its operations and hitting short-term financial targets. But Rivian isn't a value play to be judged on quarterly gross margins. It remains a venture-capital-style bet on a binary outcome, leaving investors to wonder, Is Rivian Stock a Millionaire Maker? The only data point that truly matters is the one we don't have yet: consumer demand for the R2 in 2026. Until then, everything else is just static on the line.

-

Warren Buffett's OXY Stock Play: The Latest Drama, Buffett's Angle, and Why You Shouldn't Believe the Hype

Solet'sgetthisstraight.Occide...

-

The Great Up-Leveling: What's Happening Now and How We Step Up

Haveyoueverfeltlikeyou'redri...

-

The Business of Plasma Donation: How the Process Works and Who the Key Players Are

Theterm"plasma"suffersfromas...

-

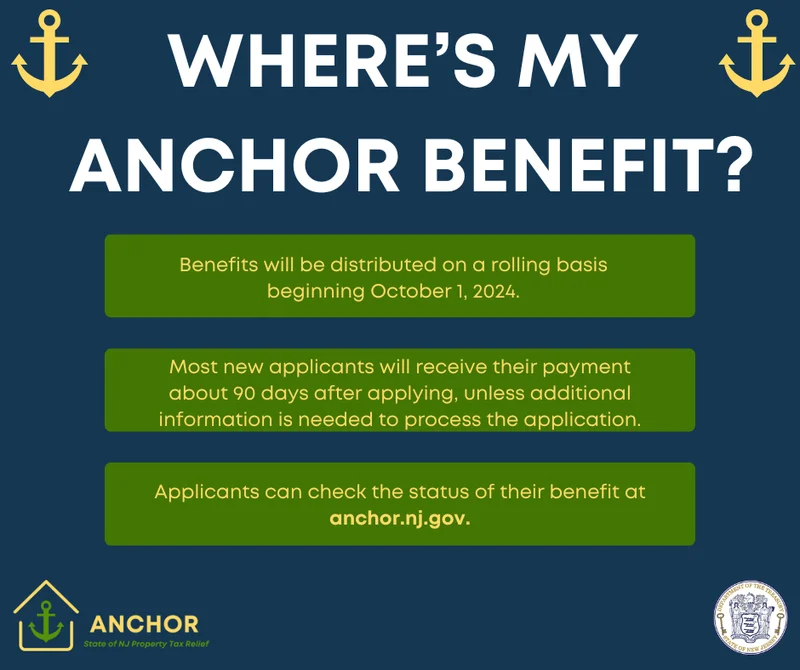

NJ's ANCHOR Program: A Blueprint for Tax Relief, Your 2024 Payment, and What Comes Next

NewJersey'sANCHORProgramIsn't...

-

The Future of Auto Parts: How to Find Any Part Instantly and What Comes Next

Walkintoany`autoparts`store—a...

- Search

- Recently Published

-

- Personal Injury Attorneys: What the Numbers Reveal About Top Firms

- Alibaba Stock: What's Driving the Price Action

- Yann LeCun: His Latest Vision and Future Insights

- BMO: Unlocking the Future of Finance, One Innovation at a Time

- The Rivian Stock Surge: An Analysis of the Rally and Its Sustainability

- Canton Network: The Hype, The Price, and The Inevitable Letdown

- WSAZ: Live News, Weather Data, and Regional Reports

- Ore: The Future of Everything?

- Monero's Privacy Surge: Price, Mining, and What the Crypto World Wants – What Reddit is Saying

- Comerica Bank: Locations, Hours, and the Quest for Customer Service

- Tag list

-

- carbon trading (2)

- Blockchain (11)

- Decentralization (5)

- Smart Contracts (4)

- Cryptocurrency (26)

- DeFi (5)

- Bitcoin (29)

- Trump (5)

- Ethereum (8)

- Pudgy Penguins (6)

- NFT (5)

- Solana (5)

- cryptocurrency (6)

- XRP (3)

- Airdrop (3)

- MicroStrategy (3)

- Stablecoin (3)

- Digital Assets (3)

- PENGU (3)

- Plasma (5)

- Zcash (6)

- Aster (4)

- investment advisor (4)

- crypto exchange binance (3)

- SX Network (3)