Snap's Stock Surge: Forecast vs. Reality

Title: Snap's Perplexity Partnership: A $400 Million Band-Aid or a Strategic Masterstroke?

Snap's stock jumped 15% on news of better-than-expected Q3 earnings and a $500 million stock repurchase program. Buried in that headline, though, is a more intriguing development: a $400 million deal with Perplexity AI. The question is, does this partnership represent a genuine strategic shift, or is it a clever financial maneuver to mask deeper problems?

The Headline Numbers vs. The Fine Print

Let's break down the headline numbers first. Revenue came in at $1.51 billion against an expected $1.49 billion. Daily active users (DAU) hit 477 million, slightly above the 476 million anticipated. Average revenue per user (ARPU) also edged up to $3.16, from the projected $3.13. These are all positive signals, no doubt. But it's crucial to look at the context. Snap shares were down 32% for the year before this announcement. A 15% jump is significant, but it barely makes a dent in the overall decline. According to a CNBC report, Snap shares rocket 15% on strong forecast, $400 million Perplexity deal.

The Perplexity deal is structured as a $400 million payment over one year, in a mix of cash and equity. Snap is touting this as a way for AI companies to connect with its user base. Evan Spiegel said Perplexity will have "default placement in our chat inbox." Sounds promising, right? But here's where the skepticism kicks in. Snap won't be selling ads against Perplexity's responses. Spiegel claims this integration will help Perplexity drive subscribers, which he thinks will be "valuable to their business."

I find this reasoning… optimistic. Snap is essentially giving away prime real estate in its app to a third-party AI, hoping that Perplexity's success will somehow trickle down to them. It's like a landlord offering a tenant free rent in exchange for the hope that the tenant's business will attract more customers to the building. It's a bet, not a guarantee. Is this a sign of desperation? Maybe.

Reading Between the Lines

Snap's Q4 sales forecast is between $1.68 billion and $1.71 billion, slightly ahead of the $1.69 billion expected by Wall Street. Adjusted EBITDA is projected at $280 million to $310 million, topping StreetAccount's $255.4 million estimate. These are good signs. But Snap's finance chief, Derek Andersen, also pointed out that North America remains a "primary headwind" to revenue growth. The company is seeing more traction with small-to-medium businesses in other regions.

Andersen's comment raises a red flag. Snap's core market—North America—is struggling. The company is relying on growth in other regions and a partnership with an AI startup to turn things around. That’s a risky proposition.

Here’s a thought leap: how reliable are Snap's DAU and ARPU metrics? The company itself acknowledges that government regulations, like Australia's social media minimum age bill, and platform-level age verification from Apple and Google could negatively impact user engagement. Utah and California have also signed online-child safety bills. All of these measures will make it harder for underage users to access Snapchat, which could lead to a decline in DAU. Snap admits that its efforts to improve monetization, such as the Snapchat+ subscription service, could also have an "adverse impact on engagement metrics." So, the very metrics driving the stock jump could be artificially inflated and about to take a hit.

I've looked at hundreds of these filings, and this level of explicit warning about potential metric declines is unusual. It suggests that Snap is bracing for impact.

The Augmented Reality Gamble

Then there's the augmented reality (AR) play. Spiegel said Snap plans to create a separate subsidiary around the Specs AR glasses to speed up development with partners. This is a long-term bet on a technology that has yet to achieve mainstream adoption. While AR has potential, it's also a capital-intensive endeavor with no guarantee of success. Snap is essentially doubling down on a high-risk, high-reward strategy.

Is This Just Window Dressing?

Snap's stock repurchase program is another interesting piece of the puzzle. The company is using $500 million to buy back its own shares. This can boost earnings per share and signal confidence to investors. But it's also a way to prop up the stock price. Is Snap using its cash to mask underlying weaknesses? It's possible. The repurchase program is a relatively small amount compared to the company's overall market cap, but it could provide a short-term boost to investor sentiment.

So, What's the Real Story?

Snap's Q3 earnings and the Perplexity partnership offer a mixed bag of signals. While the headline numbers are positive, a deeper dive reveals potential challenges and risks. The company is facing headwinds in its core market, relying on uncertain growth in other regions, and betting big on AR. The Perplexity deal could be a strategic masterstroke, but it could also be a $400 million band-aid. Only time will tell.

-

Warren Buffett's OXY Stock Play: The Latest Drama, Buffett's Angle, and Why You Shouldn't Believe the Hype

Solet'sgetthisstraight.Occide...

-

The Great Up-Leveling: What's Happening Now and How We Step Up

Haveyoueverfeltlikeyou'redri...

-

The Business of Plasma Donation: How the Process Works and Who the Key Players Are

Theterm"plasma"suffersfromas...

-

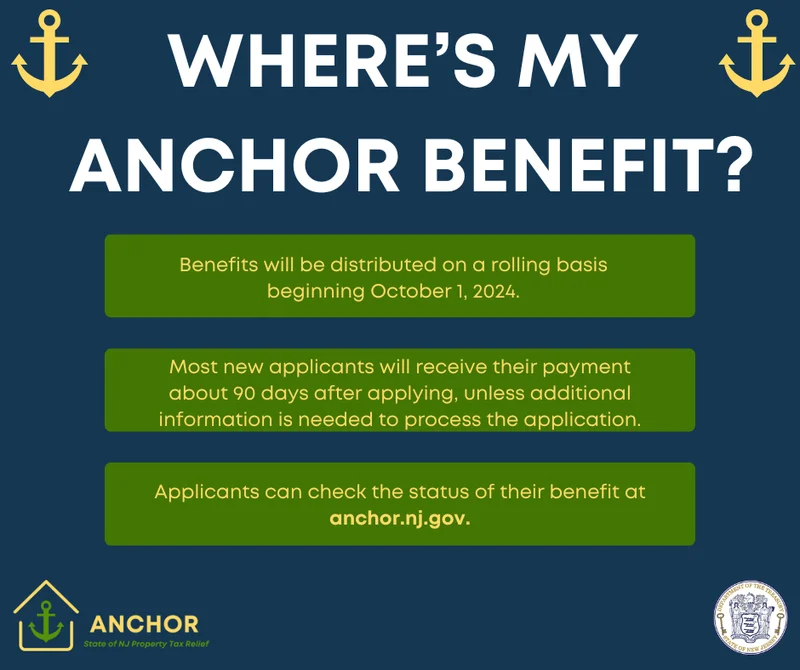

NJ's ANCHOR Program: A Blueprint for Tax Relief, Your 2024 Payment, and What Comes Next

NewJersey'sANCHORProgramIsn't...

-

The Future of Auto Parts: How to Find Any Part Instantly and What Comes Next

Walkintoany`autoparts`store—a...

- Search

- Recently Published

-

- Personal Injury Attorneys: What the Numbers Reveal About Top Firms

- Alibaba Stock: What's Driving the Price Action

- Yann LeCun: His Latest Vision and Future Insights

- BMO: Unlocking the Future of Finance, One Innovation at a Time

- The Rivian Stock Surge: An Analysis of the Rally and Its Sustainability

- Canton Network: The Hype, The Price, and The Inevitable Letdown

- WSAZ: Live News, Weather Data, and Regional Reports

- Ore: The Future of Everything?

- Monero's Privacy Surge: Price, Mining, and What the Crypto World Wants – What Reddit is Saying

- Comerica Bank: Locations, Hours, and the Quest for Customer Service

- Tag list

-

- carbon trading (2)

- Blockchain (11)

- Decentralization (5)

- Smart Contracts (4)

- Cryptocurrency (26)

- DeFi (5)

- Bitcoin (29)

- Trump (5)

- Ethereum (8)

- Pudgy Penguins (6)

- NFT (5)

- Solana (5)

- cryptocurrency (6)

- XRP (3)

- Airdrop (3)

- MicroStrategy (3)

- Stablecoin (3)

- Digital Assets (3)

- PENGU (3)

- Plasma (5)

- Zcash (6)

- Aster (4)

- investment advisor (4)

- crypto exchange binance (3)

- SX Network (3)