Nebius Q3 Earnings: Vineland Ramp vs. Full-Year Targets

Nebius (NBIS) is banking on its Vineland ramp to hit full-year targets. That’s the story, anyway. But let's dissect this "key catalyst" claim a bit. The narrative hinges on Vineland significantly boosting revenue in Q3 and Q4. Is this realistic, or are we looking at another case of hockey-stick projections that never materialize?

Examining the Vineland Hype

The core argument rests on the assumption that Vineland's increased production capacity will translate directly into increased sales. But let's not forget basic economics: production capacity doesn't equal demand. Are there confirmed orders to justify this optimism? The report doesn't explicitly state the order backlog, which is a red flag. We're expected to simply trust the company's assertion.

And here's the part of the report that I find genuinely puzzling: the lack of concrete data on Vineland's operational efficiency. What’s the current yield rate? What are the production costs per unit at Vineland? Without these figures, it's impossible to independently verify whether the ramp-up is actually profitable or just a costly exercise in increasing output.

The Insider Signal: A Grain of Salt

The author mentions insider buying as a positive sign. Agreed – it can be. But let's add some nuance. How significant was the insider buying relative to their existing holdings? Was it a token purchase to signal confidence, or a substantial investment? Also, who exactly was buying? A CEO loading up on shares sends a stronger signal than a junior VP picking up a few options. (Parenthetical clarification: I'm not saying insider buying is irrelevant, just that it requires context.)

The report highlights the author's preference for companies that have experienced a recent sell-off due to non-recurrent events. That's a valid strategy. But "non-recurrent" is a slippery term. How do we know the events truly won't recur? Supply chain disruptions, for example, have been plaguing industries for years now. Are we sure these disruptions are really behind us, or are they just temporarily subsided?

The author's disclaimer about their aeronautical engineering background being irrelevant to their investment style is amusing. But it also raises a question: are they sure it's irrelevant? Engineering principles – systems thinking, risk assessment, understanding complex processes – can be valuable in evaluating companies, even if they're not directly related to aerospace.

So, What's the Real Story?

The analysis feels more like wishful thinking than a data-driven assessment. The Vineland ramp could be the catalyst Nebius needs. But without more transparency and verifiable data, it's just another hopeful projection.

-

Warren Buffett's OXY Stock Play: The Latest Drama, Buffett's Angle, and Why You Shouldn't Believe the Hype

Solet'sgetthisstraight.Occide...

-

The Great Up-Leveling: What's Happening Now and How We Step Up

Haveyoueverfeltlikeyou'redri...

-

The Business of Plasma Donation: How the Process Works and Who the Key Players Are

Theterm"plasma"suffersfromas...

-

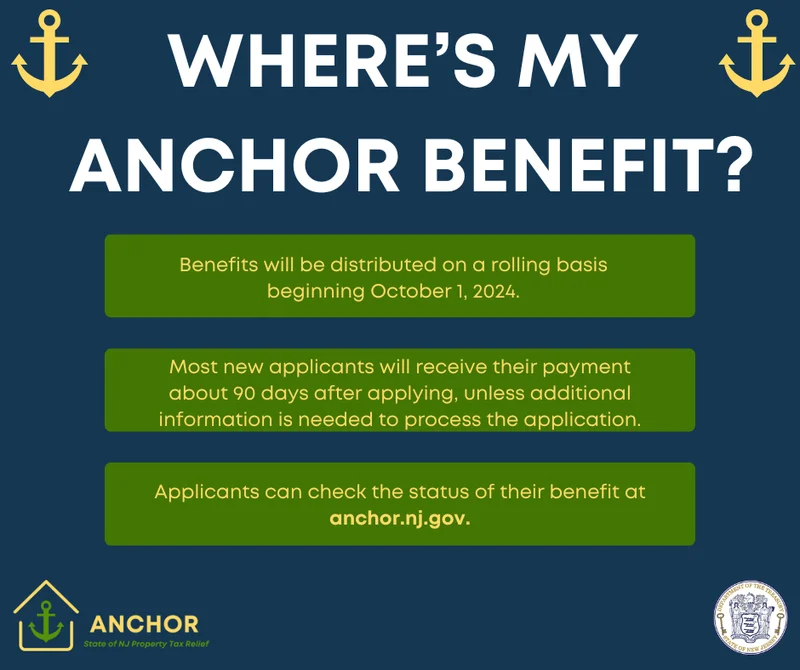

NJ's ANCHOR Program: A Blueprint for Tax Relief, Your 2024 Payment, and What Comes Next

NewJersey'sANCHORProgramIsn't...

-

The Future of Auto Parts: How to Find Any Part Instantly and What Comes Next

Walkintoany`autoparts`store—a...

- Search

- Recently Published

-

- Personal Injury Attorneys: What the Numbers Reveal About Top Firms

- Alibaba Stock: What's Driving the Price Action

- Yann LeCun: His Latest Vision and Future Insights

- BMO: Unlocking the Future of Finance, One Innovation at a Time

- The Rivian Stock Surge: An Analysis of the Rally and Its Sustainability

- Canton Network: The Hype, The Price, and The Inevitable Letdown

- WSAZ: Live News, Weather Data, and Regional Reports

- Ore: The Future of Everything?

- Monero's Privacy Surge: Price, Mining, and What the Crypto World Wants – What Reddit is Saying

- Comerica Bank: Locations, Hours, and the Quest for Customer Service

- Tag list

-

- carbon trading (2)

- Blockchain (11)

- Decentralization (5)

- Smart Contracts (4)

- Cryptocurrency (26)

- DeFi (5)

- Bitcoin (29)

- Trump (5)

- Ethereum (8)

- Pudgy Penguins (6)

- NFT (5)

- Solana (5)

- cryptocurrency (6)

- XRP (3)

- Airdrop (3)

- MicroStrategy (3)

- Stablecoin (3)

- Digital Assets (3)

- PENGU (3)

- Plasma (5)

- Zcash (6)

- Aster (4)

- investment advisor (4)

- crypto exchange binance (3)

- SX Network (3)